The US dollar is suffering from increasing pressure due to the growing divergence in expectations surrounding interest rates in the US and the eurozone. The European Central Bank is preparing for a rate increase in 2026, while the Federal Reserve plans to continue its rate cuts, creating a stark contrast for the American currency.

The swap markets expect an ECB rate increase of 0.06 percentage points by the end of 2026—a dramatic turnaround in just one week. This reflects confidence in the resilience of inflation and decent economic growth in the eurozone. At the same time, the Federal Reserve aims to ensure a "soft landing," with two more rate cuts anticipated.

Global dynamics are intensifying pressure on the dollar. Australia and Canada are considering rate hikes, and the Bank of England is expected to halt rate cuts by the summer of 2026. Analysts describe 2026 as a potential "turning point" for central banks outside the US. If the gap between interest rates narrows, demand for the low-yielding dollar could drop even further. In 2025, the currency had already fallen by more than 8% against major currencies.

Dollar faces growing pressure ahead of Christmas

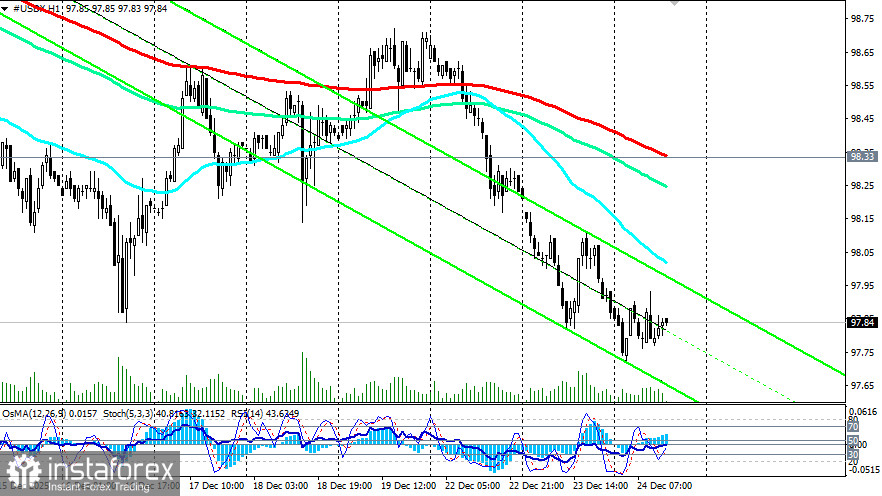

The US dollar remains under pressure ahead of Christmas. Before the opening of today's American trading session, futures on the dollar index (USDX) are trading at the closing price of the previous trading day and near the 97.85 mark.

Today, trading volumes are low as market participants prepare for the holiday season. US exchange floors are operating shorter trading hours: they will close earlier than usual and remain closed tomorrow. The holidays when Forex is closed include Christmas (December 25) and New Year (January 1). On all other business days (Monday to Friday), Forex is open, but trader activity and trading volumes will be low.

Today's economic calendar does not feature any important macroeconomic data. Reports will be released only next week and, even then, in very limited quantities. Only starting next Monday (January 5) high-priority macro data will be published.

However, traders will still pay attention to the US labor market's weekly figures being released today (at 13:30 GMT) regarding the number of jobless claims. Labor market data typically has a notable impact on dollar dynamics. A decrease in unemployment claims usually has a positive effect on the dollar, and vice versa when the figures rise.

Nonetheless, due to the pre-holiday atmosphere, the reaction to this publication will likely be short-lived, although sharp movements can still occur in a thin market.

Meanwhile, market participants are analyzing the macroeconomic statistics released yesterday. For instance, the US Bureau of Economic Analysis reported on Tuesday that the country's GDP grew by 4.3% (year-over-year) in the third quarter, significantly above market forecasts of 3.3% and an acceleration from the 3.8% growth seen in the second quarter. The core PCE price index increased by 2.9% compared to the previous quarter, aligning with expectations.

The markets reacted mixed: the dollar initially surged from daily lows but then pulled back and remained steady below the 98.00 mark after a weekly decline of around 1%. Other macro data revealed that durable goods orders fell by 2.2% month-over-month in October, while industrial production increased by 0.2% in November.

Political and monetary comments added uncertainty. President Donald Trump stated on social media that critics would not be able to lead the Federal Reserve and expressed a desire for the new chair to lower interest rates given favorable conditions. White House advisor Kevin Hassett noted that the Fed is not lowering rates fast enough in light of stronger-than-expected economic growth. Meanwhile, Fed officials, including Board member Stephen Mirando, indicate a gradual reduction in disagreements regarding future rate cuts.

The CME FedWatch tool assesses the likelihood of rate cuts in 2026 at around 70%, with market participants pricing in two rate cuts, despite positive economic data. However, preliminary estimates suggest that any rate cuts will occur gradually rather than abruptly.

Conclusions and outlook

Thus, the US economy demonstrates decent economic growth rates, although the recovery is uneven. Positive dynamics are largely linked to increased business investments in new technologies and equipment, particularly in the field of artificial intelligence. At the same time, consumer spending, especially among low- and middle-income households, remains weak due to rising inflationary risks and a lack of new job creation.

The US economy is firmly on path to recovery, but its future trajectory depends on many factors, including global trade relationships, domestic monetary policy, and the state of labor and capital markets. Further dollar weakening is forecasted, while economists anticipate weaker GDP figures in the fourth quarter, as the government shutdown may have negatively impacted the economy.

The dollar's decline could either accelerate or slow down, depending on the results of upcoming macroeconomic data releases.